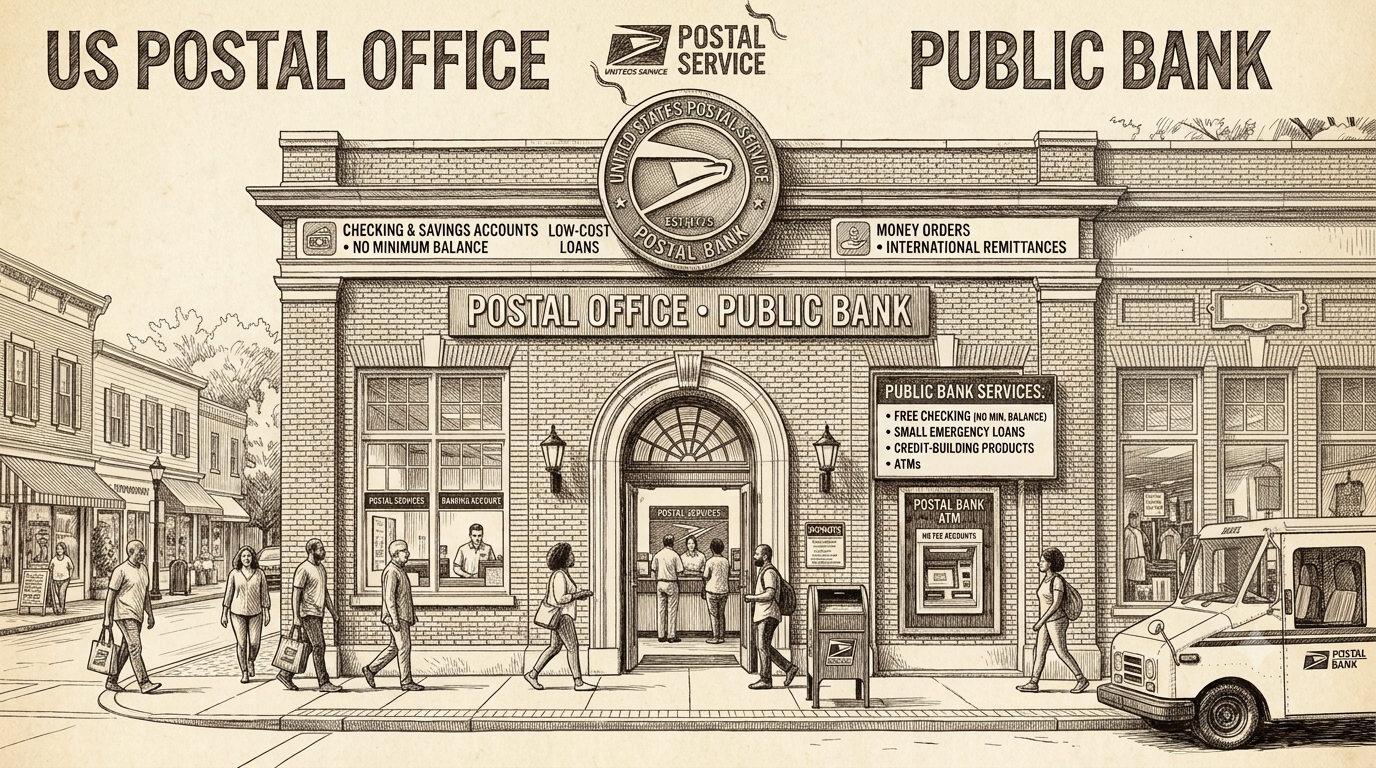

Why not make the post office a public bank?

Welcome to our series dedicated to creating and sharing innovative policy ideas that can have direct material benefit to people.

Today we talk about banking.

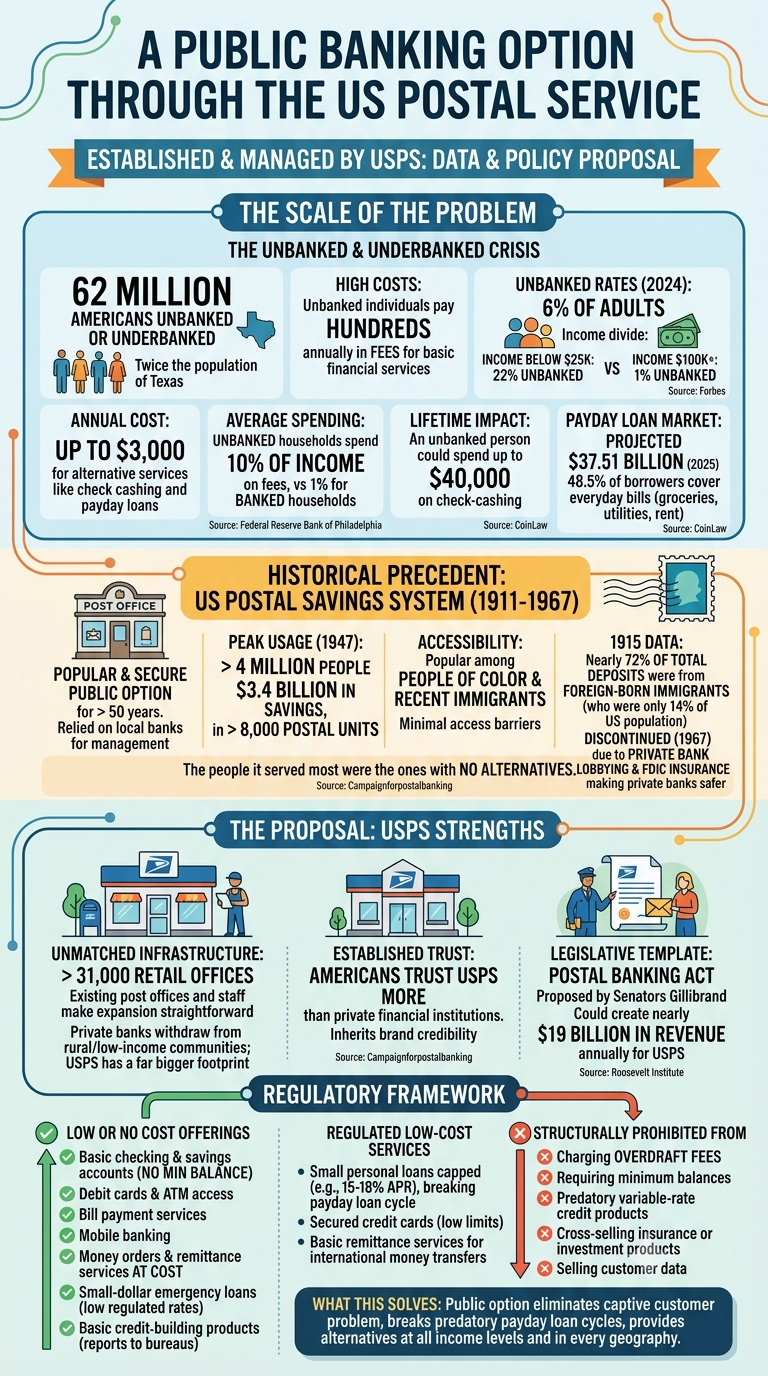

Did you know over 62 million Americans currently do not have access to banking services, equivalent to twice the population of Texas? These households pay hundreds of dollars annually in fees just to access basic financial services, money that could otherwise go toward rent, food, or education.

6% of adults were unbanked in 2024, meaning neither they nor their spouse or partner had a checking, savings, or money market account.

Being unbanked costs individuals up to $3,000 annually in fees for alternative financial services like check cashing and payday loans. Unbanked households in the US spend 10% of their income on financial transaction fees, compared to just 1% for banked households.

The United States Postal Bank is a proposed public option that would allow the U.S. Postal Service to offer basic financial services to all Americans. This system would utilize the existing footprint of over 31,000 post offices to provide essential resources like checking accounts, savings accounts, and low-interest emergency loans.

By establishing a postal bank system, we create access to opportunity for millions of Americans who currently lack access to traditional financial institutions. Operating as a nonprofit utility, the system is designed to eliminate predatory financial fees and serve all communities.

Historically Popular, Discontinued due to outside Corruption

The US successfully operated a hugely popular and secure public banking option through the Postal Service for more than 50 years. Created in 1911 before the Fed was founded, the Postal Savings System relied on local banks to manage accounts and allowed all Americans to make deposits into no-cost savings accounts at post offices. By 1947, more than 4 million people had $3.4 billion in savings in more than 8,000 postal units.

The Postal Savings System had minimal access barriers, making it particularly popular.

The system was eventually discontinued in 1967 because private banks had lobbied against it from its founding.

Bankers used their political leverage to bake fatal competitive restrictions into the Postal Savings System Act of 1910:

2% Interest Cap: Bankers successfully lobbied Congress to legally freeze the postal bank’s interest rate at a low 2%. Commercial banks at the time paid around 3.5%, ensuring the post office could never out-compete private banks for affluent customers.

Deposit Limit: They successfully capped maximum individual balances at an incredibly low $500 to guarantee the post office could only serve low-income individuals and never attract the lucrative wealth of the middle or upper classes.

Redeposit Concession: In a massive win for Wall Street, lobbying forced the post office to redeposit 95% of its cash right back into local private commercial banks at a cheap 2.25% interest rate. Essentially, private banks forced the government to act as a low-cost capital funnel for their own private lending operations.

A successful revival of the Postal Banking system would require it to have control over its capabilities to provide banking services to all Americans. And prevent the corrupted limitations of the past.

Small Business Community Banking

For decades, small businesses have been ignored by national policy, which has favored homogenizing our economic ecosystem for the largest of companies.A public postal bank would benefit small businesses by expanding opportunities by offering specialized commercial accounts and capital tools to support local entrepreneurs. This framework introduces fee-free commercial checking and basic merchant processing services to protect mom-and-pop shops from high transaction fees. These business capabilities are designed to fill critical credit gaps in commercial banking deserts where private institutions have shut down physical branches.

Imagine transactional services similar to Cash App and PayPal without the transaction fees that can help small businesses grow.

By providing no-fee transactions and micro-loans with low, fixed interest rates, the system ensures small businesses can reliably fund inventory and equipment. The postal bank would also partner with local Community Development Financial Institutions to efficiently distribute capital into neighborhood economies.

This strategic expansion transforms the post office into a vital driver of localized economic growth and stability. Ultimately, integrating business banking creates a self-sustaining circular economy that keeps wealth directly within the community.

What are your thoughts on this policy idea?